Earn 9%–15% on Senior Secured Bonds.

Lower risk. Fixed returns. Start investing on Aspero with just ₹10,000.

Explore Bonds

When it comes to investing your hard-earned money, it’s important to choose an option that is safe, reliable, and offers good returns. Two of the most popular investment options for risk-averse investors are bonds and fixed deposits.

These are both low-risk investment options and offer fixed returns, but they have some key differences. Let’s take a closer look at each option, the differences between the two and help you decide which one might be the best for your investment goals.

Bonds: High return & a hedge against inflation

Bonds are a type of debt instrument issued by companies, governments, and other organizations to raise funds. In other words, bonds are loans made by investors to these entities, who in turn promise to repay the principal amount along with interest. Bonds have a fixed maturity date, after which the principal amount is repaid to the investor. The interest rate on bonds is fixed at the time of issuance, and it is paid to the investor either periodically or at the time of maturity.

Fixed Deposits: Secure and Guaranteed returns

Fixed deposits are a type of investment option offered by banks and financial institutions. When an investor opens a fixed deposit account, they deposit a lump sum of money with the bank for a fixed period, ranging from a few months to several years. The bank pays a fixed rate of interest on the deposit, which is usually higher than the interest rate offered on savings accounts.

Fixed deposits are considered a low-risk investment option since the investor is guaranteed to receive the principal amount and the interest rate on maturity. Additionally, fixed deposits are insured by the Deposit Insurance and Credit Guarantee Corporation of India (DICGC), which offers a deposit insurance cover of up to Rs. 5 lakh per depositor per bank.

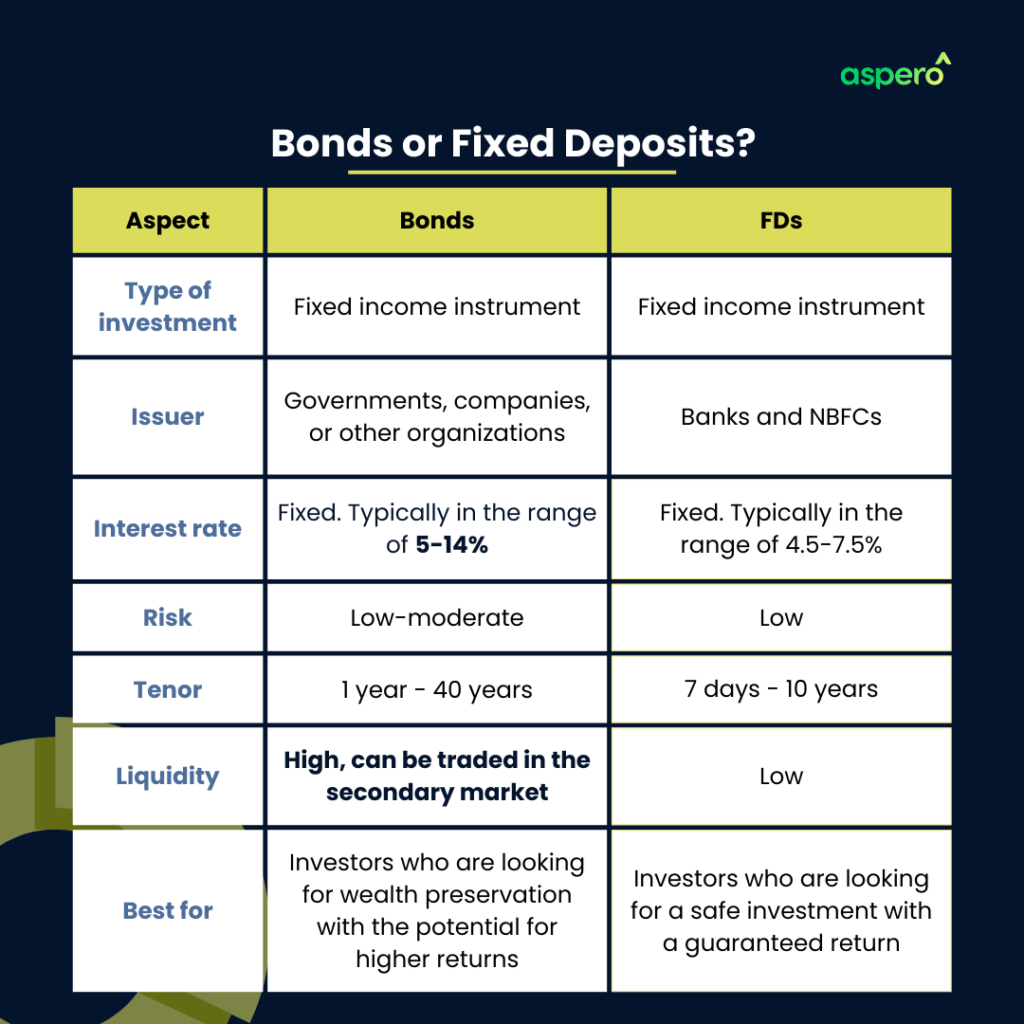

Bonds vs Fixed Deposits

While both bonds and fixed deposits are low-risk investment options that offer a fixed return, there are several differences between the two investment options that investors should consider before investing.

1. Issuer:

Bonds are issued by corporations, governments, and municipalities, while fixed deposits are issued by banks and NBFCs.

2. Interest rate:

The interest rate on bonds is typically higher than the interest rate offered on fixed deposits since bonds are considered riskier than fixed deposits. The higher interest rate compensates the investor for the credit risk associated with the bond. The interest rate on fixed deposits is fixed for the entire tenure of the deposit, meaning that the investor will receive the same rate of return throughout the investment period. However, the interest rate on bonds may vary depending on market conditions, making them relatively more volatile than fixed deposits.

3. Tenure:

The tenure of an investment is an important factor to consider when choosing between bonds and fixed deposits. Fixed deposits offer a range of tenures, from ultra-short tenures of 7-14 days to a maximum of 10 years. Tax-saving fixed deposits have a lock-in period of 5 years during which the investor cannot withdraw the investment.

On the other hand, bonds have tenures that depend on the issuer. The Government of India issues bonds for tenures ranging from 5 to 40 years, while companies may issue bonds for shorter or longer periods based on their purpose and target amount. The longer tenure of bonds may provide an opportunity for investors to earn higher returns, but it also comes with the risk of lesser liquidity and flexibility.

4. Liquidity:

Liquidity is an important factor to consider when choosing between fixed deposits and bonds. Fixed deposit liquidity depends largely on the tenure of the deposit. Short-term fixed deposits, with tenures ranging from a few days to a few months, offer higher liquidity as the investor can recover their principal quickly. However, longer-tenure fixed deposits require the principal to be tied up for a longer period, reducing liquidity. In case an investor requires sudden liquidity, they can prematurely withdraw their fixed deposit. However, this may result in the loss of future interest and the imposition of a penalty by the bank.

On the other hand, bonds that are frequently traded or traded at high volumes on a stock exchange will have stronger liquidity, allowing the investor to easily sell them for cash. However, other bonds may be less liquid, making it harder to sell them. All bonds are subject to liquidity risk, meaning that an investor may not always receive a price reflective of its true value. Furthermore, bond liquidity comes at the cost of market volatility since interest rate movements in the market impact bond prices and the ultimate price an investor will get for selling the bond.

5. Credit risk:

Bonds are subject to credit risk since they are backed by the creditworthiness of the issuer. If the issuer defaults on the loan, the investor may lose their principal amount and interest. Hence the creditworthiness of the issuer becomes a critical factor in evaluating bonds.

Fixed deposits in banks are generally considered to be a low-risk investment option as they are not subject to market fluctuations. However, it is important to note that all banks carry some level of financial risk, and in the event of a bank’s insolvency, there is a risk of losing the invested funds. However, FDs are insured by the Deposit Insurance and Credit Guarantee Corporation of India (DICGC), which offers a deposit insurance cover of up to Rs. 5 lakh per depositor per bank. This insurance cover provides investors with a safety net, protecting their investment against default risk.

6. Credit Ratings:

Credit rating agencies such as CRISIL, ICRA, and CARE provide credit ratings to bonds and FDs issued by NBFCs.

The credit rating assigned to a bond can range from investment grade to junk, and bond issuers are required to specify the rating when issuing a bond to potential investors. In contrast, banks are not required to provide credit ratings for their FDs.

Different rating agencies use different scales to rate a bond as investment-grade (low risk), junk (high risk), or somewhere in between (moderate risk).

Should you Invest in Bonds or Fixed Deposits?

Deciding whether to invest in bonds or fixed deposits depends on an individual’s investment goals, risk tolerance, and investment horizon. Fixed deposits are a low-risk investment option suitable for short-term goals or those looking for a fixed income stream. They offer a guaranteed return of principal and interest and are backed by deposit insurance. On the other hand, bonds offer higher returns but come with a slightly higher risk of default, market volatility, and interest rate risk. They are more suitable for investors with some risk tolerance.

Ultimately, the decision to invest in bonds or fixed deposits should be based on individual circumstances and financial goals. It is important to carefully consider the risks and returns associated with each investment option and seek professional advice if needed.

Aspero

We hope you understand the difference between fixed deposits and bonds. Consider all the factors, your goals, and risk appetite and invest wisely.

If bonds seem like a better choice for you right now, explore Aspero. Your smart investment platform for fixed-income securities. Discover a wide array of exclusive bonds and earn steady returns up to 11%