Earn 9%–15% on Senior Secured Bonds.

Lower risk. Fixed returns. Start investing on Aspero with just ₹10,000.

Explore Bonds

Introduction to bond taxation in India

In the realm of finance, bonds serve as a popular investment option, providing stability and fixed income to investors. However, comprehending the taxation rules surrounding bonds in India can be a complex task. This comprehensive guide aims to shed light on everything you need to know about bond taxation in India, enabling you to make well-informed investment decisions.

Understanding Bonds

Before diving into bond taxation, let’s briefly revisit the basics of bonds. In India, bonds represent fixed-income instruments where investors lend money to issuers such as the government, financial institutions, or corporations. The issuer commits to regular interest payments (coupon payments) to bondholders until the bond matures, at which point the principal amount is repaid.

Investing in tax-advantaged accounts like PPF or tax-saving FDs for bonds can offer tax benefits in India. Interest earned in these accounts is usually tax-exempt or tax-deferred, with certain limits and conditions.

Taxation of Bond Discounts and Premiums

When bonds are traded in the secondary market, they may be priced above or below their face value. This leads to two scenarios related to taxation:

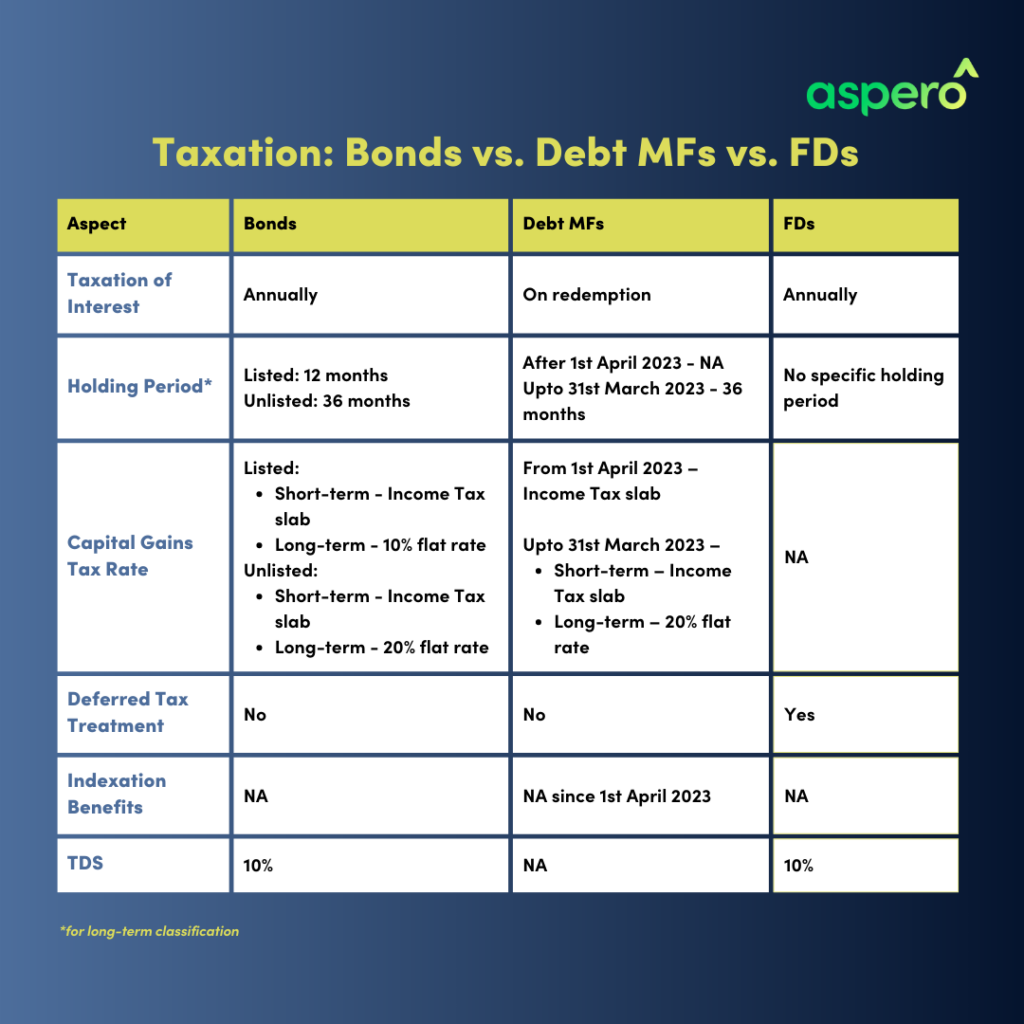

a. Bond Discounts: If a bond is purchased at a price below its face value, the discount represents the difference between the purchase price and the face value. The discount is generally considered as interest income and taxed as per the applicable income tax slab rates.

b. Bond Premiums: Conversely, if a bond is purchased at a price above its face value, the premium paid has no tax implications. However, the premium amount does not qualify for deductions or exemptions while computing the taxable income.

c. Zero Coupon Bonds (ZCB): As the name indicates, these bonds do not pay coupon / interest during their tenure. Instead, the instrument is offered at a discounted price during issue and redeemed at face value during the end of its tenure. The returns to an investor of ZCB would only be in the form of capital appreciation. These gains are taxed as short-term capital gains (taxable at slab rates) or long-term capital gains (taxable either at 10% without indexation benefit, or 20% with indexation benefit), depending on the holding period criteria (12 months).

Taxation of Bond Maturities and Sales

When a bond matures or is sold before maturity, there are tax implications to consider:

a. Maturity: Upon bond maturity, the investor receives the principal amount, which is tax-free. However, any accrued interest earned over the bond’s term is considered as interest income and taxed at the applicable income tax slab rates.

b. Early Redemption/Sale: If a bond is sold before maturity, any capital gains or losses realized are subject to taxation. Capital gains on bonds held for less than 36 months are classified as short-term capital gains (STCG) and taxed at the applicable income tax slab rates. Bonds held for more than 36 months are considered long-term capital assets, and capital gains are taxed at a flat rate of 20% without indexation benefits.

Tax-Efficient Portfolio Strategy

You can strategically utilize the concept of booking capital gains on debt products such as bonds and combine it with booking losses on your shares or mutual funds to neutralize the capital gains tax on your overall portfolio potentially. This strategy, known as tax-loss harvesting or tax-efficient portfolio management, allows you to optimize your tax liability.

Tax-loss harvesting involves selling investments that have experienced losses to offset the capital gains made from selling other investments that have appreciated in value. By doing so, you can potentially reduce your overall tax liability by offsetting gains with losses, effectively neutralizing the impact of capital gains tax.

When it comes to debt products like bonds, if you have realized capital gains from selling bonds, consider looking at your equity investments, such as shares or mutual funds, for any investments that have experienced losses. By strategically selling those underperforming investments, you can generate capital losses that can be used to offset the capital gains made from selling bonds.

Remember that there are certain rules and limitations regarding tax-loss harvesting. In India, the Income Tax Act specifies that long-term capital losses can only be set off against long-term capital gains, while short-term capital losses can be set off against short-term and long-term capital gains. Additionally, there are rules regarding the carry-forward and set-off of losses from previous years.

Seeking Professional Advice

Given the complexity of bond taxation in India, seeking guidance from a qualified tax professional is highly recommended. They can help ensure compliance with tax regulations, optimize your tax strategy, and provide personalized advice based on your financial situation.

Conclusion

Understanding the taxation rules surrounding bonds in India is crucial for maximizing investment returns while maintaining tax compliance. By grasping the key concepts discussed in this comprehensive guide, investors can navigate the complexities of bond taxation more confidently. Remember to stay informed and seek professional advice to make well-informed investment decisions within the realm of bonds in India.