Earn 9%–15% on Senior Secured Bonds.

Lower risk. Fixed returns. Start investing on Aspero with just ₹10,000.

Explore Bonds

Introduction

Bonds are financial instruments that offer a way to invest money and earn a fixed income over a certain period. However, it’s important to understand the basics of bond taxation, even if you’re new to the world of fixed income investments. This beginner’s guide aims to provide a clear and simple explanation of bond taxation, helping you make informed investment decisions.

What are Bonds?

Bonds are like loans where you lend money to governments, companies, or other organizations. In return, they promise to pay you back the loan amount (principal) along with regular interest payments over a specific period.

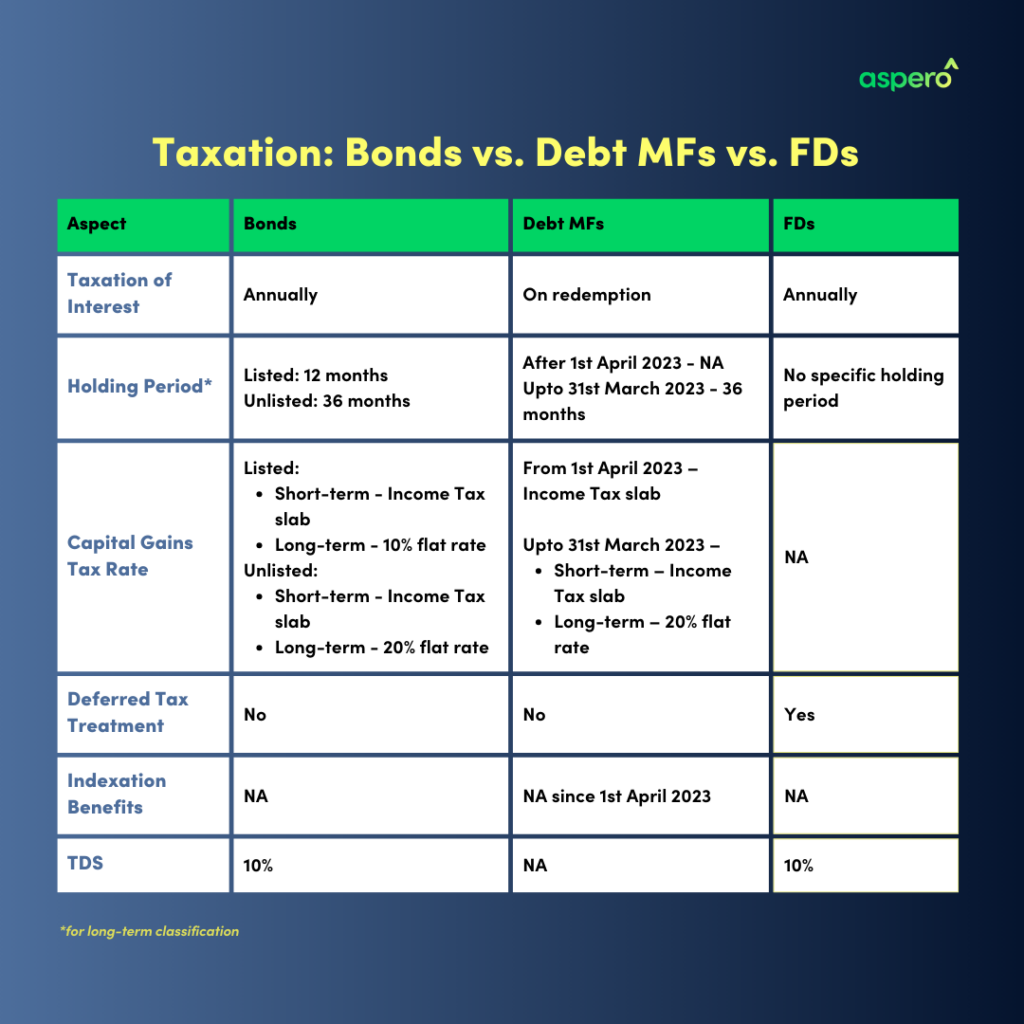

Taxation of Bond Interest

The interest income you earn from bonds is subject to taxation. Here’s what you need to know:

a. Taxable Bonds: Most bonds fall into this category, including corporate bonds and government bonds. The interest you earn from these bonds is added to your total income and taxed at the applicable income tax rates.

b. Tax-Exempt Bonds: Some bonds, like certain government-issued infrastructure bonds, may provide tax-exempt interest income. This means you don’t have to pay income tax on the interest you earn from these bonds.

Example: Suppose you have invested in a corporate bond and a tax-exempt municipal bond. Let’s assume both bonds provide an annual interest income of ₹10,000.

Taxable Bond: If you are in the 20% income tax bracket, you must pay ₹2,000 (20% of ₹10,000) as income tax on the interest earned from the corporate bond.

Tax-Exempt Bond: In the case of a tax-exempt municipal bond, you would not have to pay any income tax on the ₹10,000 interest income, resulting in tax savings.

Bond Discounts and Premiums

When bonds are bought or sold, they may be priced differently than their face value. Here’s how it affects taxation:

a. Bond Discounts: If you buy a bond at a price lower than its face value, the difference is called a discount. The discount is considered as capital gains and taxed at the applicable income tax rates.

Example: Suppose you purchase a bond with a face value of ₹10,000 at a discount of 10%. This means you buy the bond for ₹9,000. The discount of ₹1,000 (₹10,000 face value – ₹9,000 purchase price) is considered as interest income. If you are in the 15% income tax bracket, you will pay ₹150 (15% of ₹1,000) as income tax on the bond discount.

b. Bond Premiums: If you buy a bond at a price higher than its face value, the extra amount you pay is called a premium. The premium doesn’t have any immediate tax implications, but it’s not eligible for any deductions or exemptions when calculating taxable income.

Example: If you purchase a bond with a face value of ₹10,000 at a premium of 10%, meaning you buy the bond for ₹11,000. The premium of ₹1,000 has no immediate tax implications. However, it cannot be used as a deduction or exemption when calculating taxable income.

Maturity and Sales

When a bond matures or is sold before maturity, there are tax implications to consider:

a. Maturity: When a bond matures, you receive the loan amount back (principal), which is tax-free. However, any interest you earned over the bond’s term is considered as interest income and taxed at the applicable income tax rates.

Example: Suppose you hold a three-year bond with an annual interest income of ₹5,000. At the end of the third year, the bond matures, and you receive the principal amount of ₹50,000. The principal amount of ₹50,000 is tax-free. However, the accumulated interest of ₹15,000 (₹5,000 per year for three years) is considered as interest income and subject to income tax based on your applicable tax rate.

b. Early Redemption/Sale: If you sell a bond before it matures, any profit or loss from the sale is subject to taxation. If you held the bond for less than a certain period, any profit is considered short-term and taxed at the applicable income tax rates. If you held the bond for a longer period, any profit is considered long-term and taxed at a special rate.

Example: Now, suppose you sell a bond before maturity for ₹22,000, which you originally purchased for ₹20,000. The ₹2,000 profit (₹22,000 sale price – ₹20,000 purchase price) is considered a capital gain. If you held the bond for less than a year, it would be treated as a short-term capital gain and taxed at the applicable income tax rates. If you held it for more than a year, it would be considered a long-term capital gain, with a special tax rate applicable.

Tax Reporting

To accurately report bond-related income and deductions, you need to be aware of the following tax forms:

a. Form 26AS: This form shows the tax deducted at source (TDS) on the interest income you earn from bonds. You can use it to verify the TDS deducted by the issuer.

b. Form 15G/15H: These forms are used to declare that your total income is below the taxable limit. By submitting these forms to the bond issuer, you can exempt them from deducting TDS from your interest income.

c. Schedule CG: This schedule is part of the income tax return (ITR) form and is used to report any profit or loss from the sale of bonds.

As per Section 193 of the Income Tax Act, 1961, all interest income from securities, including bonds, will be subject to Tax Deducted at Source (TDS). The new TDS rate for bond interest income is 10%, applicable to listed and unlisted bonds (listed bonds included with effect from 1st April 2023). This means the bond issuer will deduct 10% of the interest income as TDS before paying the investor. The TDS deducted represents a prepayment of the income tax liability, and the actual tax liability will be determined when filing the income tax return.

Seek Professional Advice

Since bond taxation can be complex, it’s always a good idea to consult a qualified tax professional. They can provide personalized advice, ensure compliance with tax regulations, and help optimize your tax strategy.

Conclusion

Understanding bond taxation is essential for making informed investment decisions. By grasping the basic concepts discussed in this beginner’s guide, you can navigate bond taxation with confidence. Remember, if you have any doubts or need assistance, consult a tax professional to ensure you comply with tax rules and make the most of your bond investments.